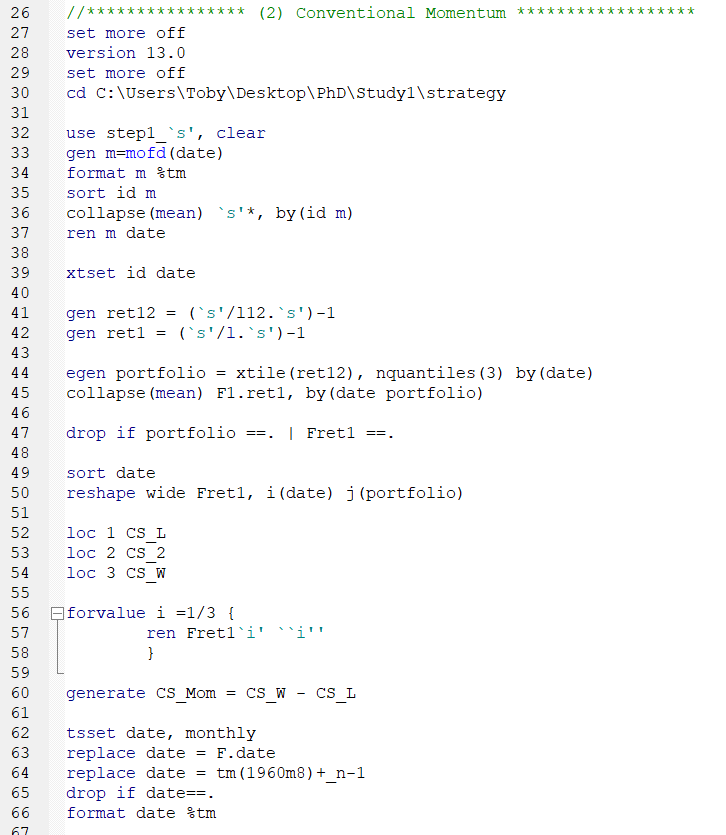

Contract Rolling

Once the time series of price observations had been compiled, it was then necessary to code a contract rolling methodology, to simulate the price and roll yield effects of holding a continuous exposure to contracts at intervals (namely, nearest and next nearest to expiry) across the futures curve.

To achieve this, the study utilises methodologies from derived from prior studies in the academic literature. In effect, I constructed a an executable DoFile to roll price observations over the nearest contract on the last trading day of the last full month prior to expiry.

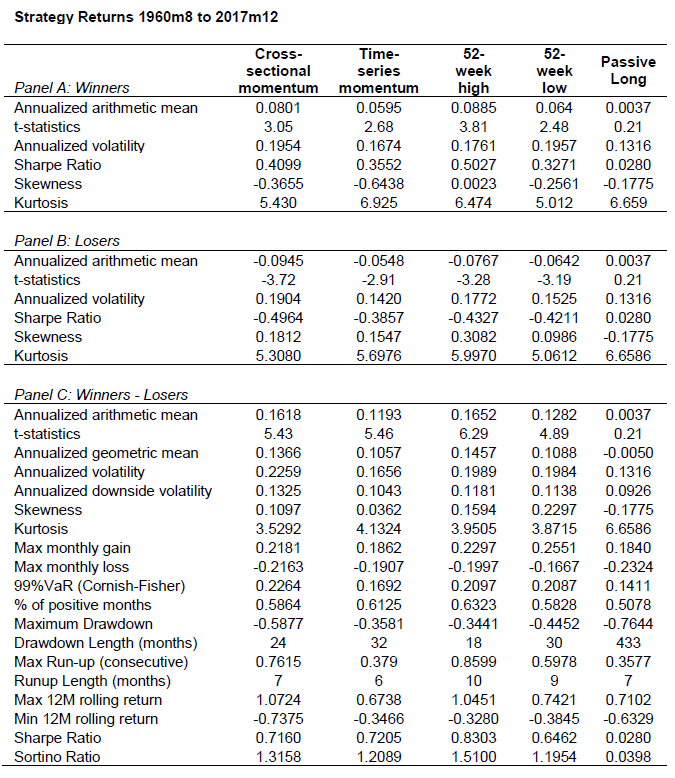

Using these rolled time series outputs, I was able to calculate descriptive statistics for monthly returns for each commodity, which you will see in the image on the left.

Click here to download an example of the code which I wrote to complete this task.