{kind=link}

{kind=link}

{kind=link}

SMAs & BBs: A Retail Investor's Quant Strategy

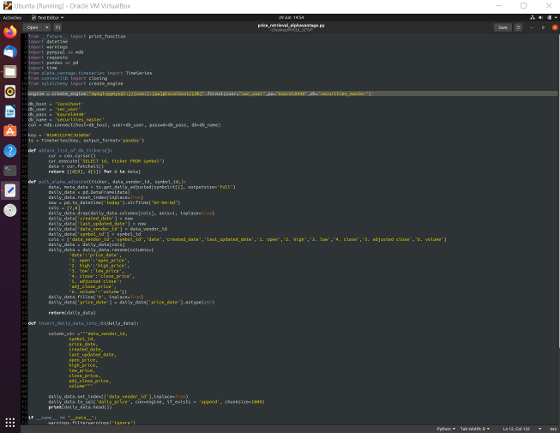

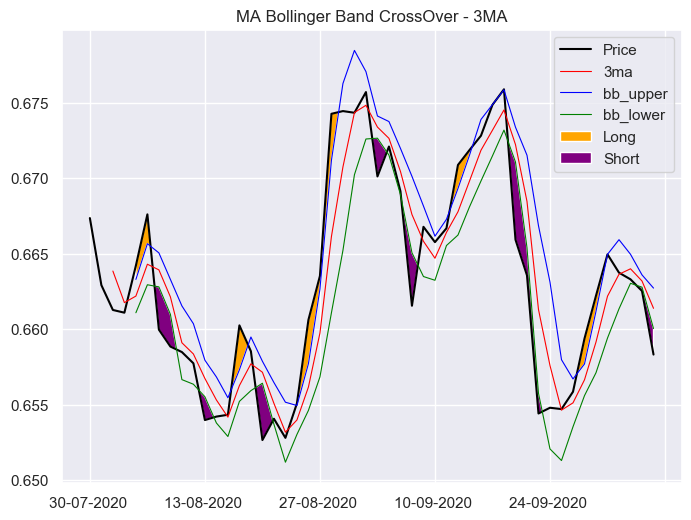

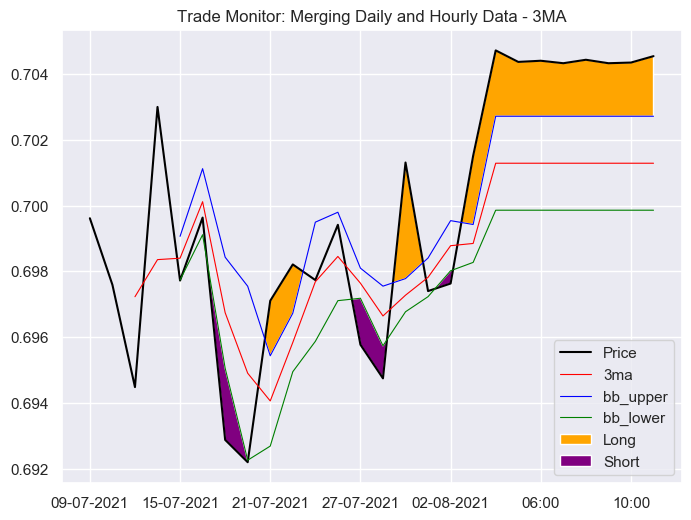

Using the API provided by Interactive Brokers, I was interested to construct and backtest a simple trend based strategy. Moving average indictors have a long history of application among technical analysts and can be useful for identfying price trends, breakouts and reversions. Motivated by the simplicity of this indicator, I downloaded daily OHLC observations for FOREX NZD/USD (chosen at random for the sake of development) trading pairs from July 2007 to July 2021. Using the Closing price series, I overlayed Arithmetic Simple Moving Average lines (rolling period average, MA hereafter) and Upper and Lower Bollinger Bands (BB hereafter) of the MA. Refer to the following notation, where sigma denotes standard deviation and x bar denotes arithmetic mean. Upper BB = (MA + 2 * sigma); MA = (rolling 3 period x bar); Lower BB = (MA - 2 * sigma)

Using these indicators I constructed trading signal rules: Long (Depicted in Orange) when the price crosses above the Upper BB (Blue Line), and Short (Depicted in Purple) when the price crosses below the Lower BB (Green Line). Intuitively, the strategy should be able to capture returns from persisting upward and downward trends in the price series, whilst remaining neutral during periods of sideward ranging price movement (i.e. within the bounds of Upper and Lower BBs).

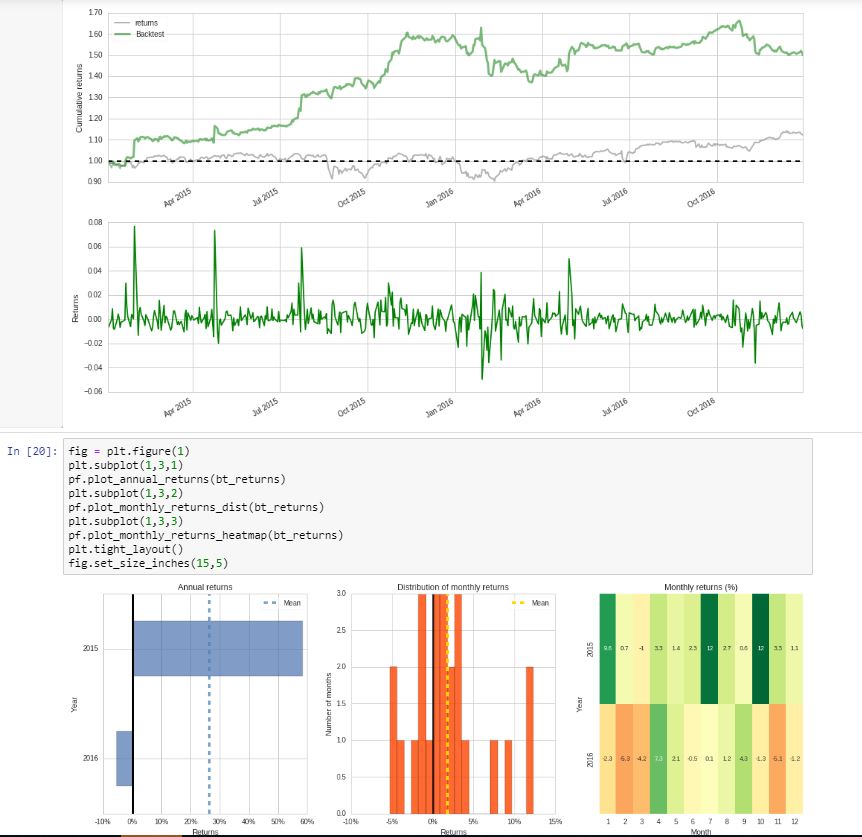

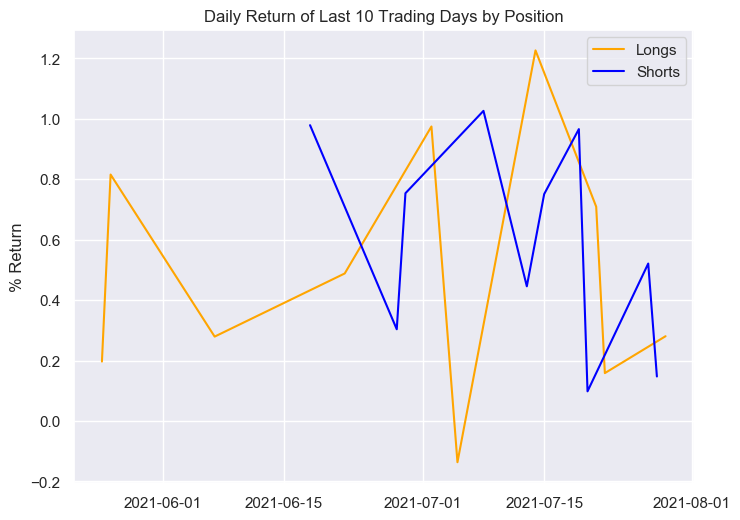

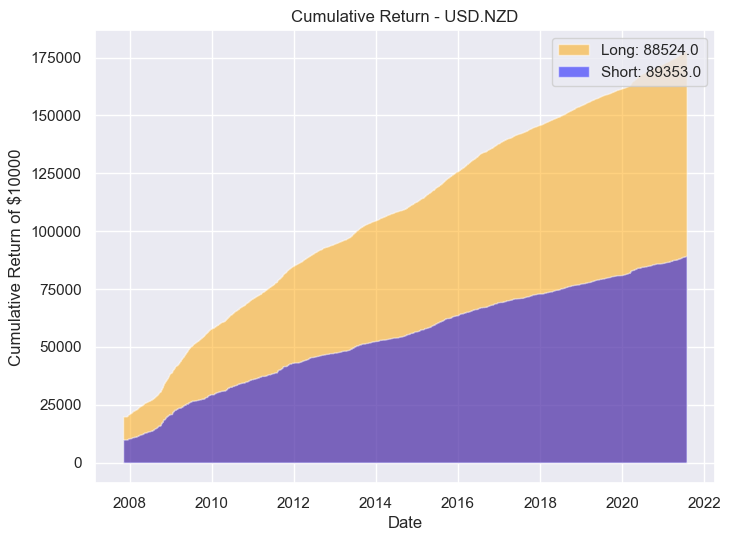

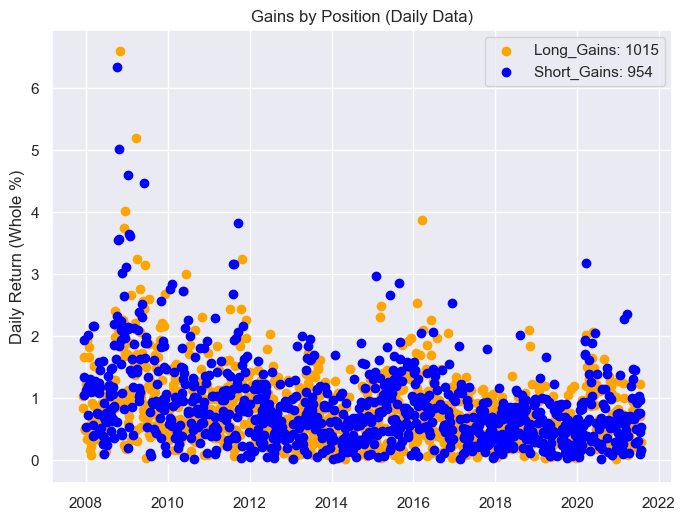

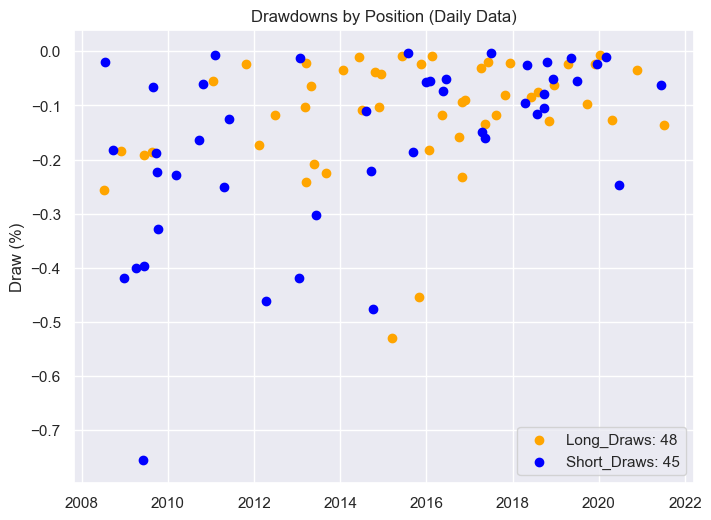

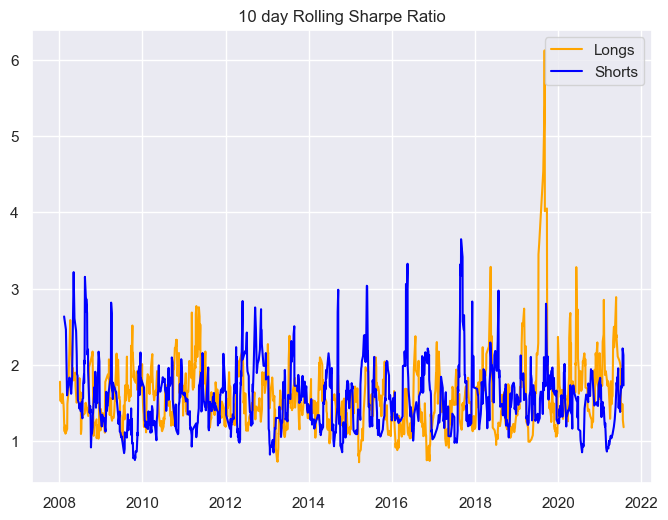

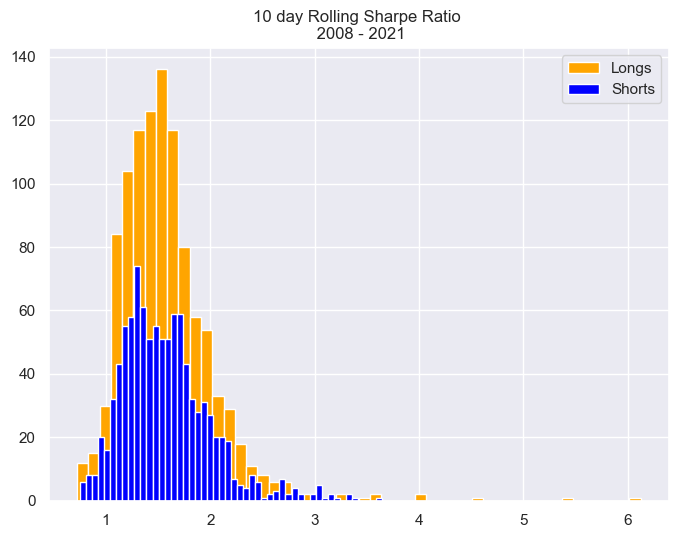

From here, we can collect and analyse the persistence, volatility and risk adjusted return components generated by each position through time. From the statical summary, we note strong significant daily returns approximating 0.8%, Sharpe exceeding 1.15, Sortino at a stagering 6.9 and 4.8 respectively, and a 99% VaR at -0.11 and -0.17. Reviewing the cumulative returns and rolling Sharpe plots, we note a strong persistency in positive returns with negligable drawdown periods (almost a perfectly straight slope in the cumulative series). Investigating further, we examine the drawdowns and extrapolate the VaR metric to measure the potential tail risk over a 100 day investment period and confirm negligable impact from drawdowns, approximating ~0.12% daily over the 49 draws and ~0.17% over 45 draws, respectively.

But could it all be too good to be true? Like many skeptics out there, when presented with results that appear 'too good to be true', my mind wonders what went wrong? What are the real risks to a strategy like this? What are the drivers and dependents for performance? Interestingly, if we examine the distribution of Holding Periods for trades in each position, we note that ~48% of all trades last only 1 day and the longest trades approximate only 4 days. This relatively high frequency suggests high transaction costs and a considerable risk of slippage at the execution end, which are not effectively captured by the analytics from this project.

The next logical step to examine effectiveness of this strategy, would be found in the PnL review from deployment to a paper trade account, which is currently in development.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}